The Financial Rocket Ship of Women's Football

They grow up so fast! Or do they?

As long as I can remember as a sports fan, women’s sports have been treated more as a curiosity or a niche-within-a-niche than as a legitimate entertainment product. Recreational play for girls and women is common, at least in the US, but professionalism - people paying to watch women play sports, in enough numbers that they can make their living doing it - has had a long winding road to respectability, with lots of bumps, roadblocks, and even a few crashes along the way. But that appears to be changing in a big way right now, in one particular area: Soccer. And I find that, personally, very exciting.

The TLDR

This article is long and detailed, because I haven’t seen this stuff laid out anywhere so I had to dig and compile a lot of it. Here are the main takeaways:

Within the last 2-3 years, Women’s Football is seeing a surge of interest, which has caused it to cross the chasm from “curiosity / niche” to “sustainable business venture”. The sporting world has not yet caught on to this new reality.

There are only 10-12 countries’ leagues globally which are fully professional, of which 8 have enough data and operating history to be analyzed.

Among those, the English WSL gets the most press, but the USA’s NWSL is absolutely kicking its butt and taking its lunch money, in every indicator that matters: Fan attendance, club revenue, broadcasting rights/reach, team valuation.

The NWSL generated $112M in revenue last year, before their big $60M/yr TV deal, roughly 3x that of the WSL, with over twice the attendance.

The biggest challenger to the NWSL for global leadership may not even be the WSL: by attendance numbers, Mexico’s Liga MX Femenil is #2 and fast growing.

I won’t get into payrolls, CBAs or the national team here; this is about how the club teams are doing financially. Which is, in a word, awesome. In most places, at least.

Edit 1/24: this report has been updated to include data from Deloitte’s new survey.

Why do I care? Why should anyone?

Firstly on a personal level, I care a lot about a few aspects of this subject. I want to see women’s football1 rise into the pantheon of sports followings and cultural awareness, both domestically and globally, for a few reasons:

I’m believer in the power of football to bring communities together and bridge gaps and heal wounds. I don’t care how sappy that sounds. FIFA exaggerates this for self-serving reasons all the time, but it really does happen in the real world (and not just in football), and in less-dramatic ways sports can facilitate cultural understanding and bond-building that’s invisible, but still real.

Sports are an emotionally evocative way to demonstrate national character, and I’d like part of our national character to (continue to) be one where women are given equal voice and attention and respect. And lots of other countries could stand to demonstrate (or learn) such things too. The world would be a better place if women are celebrated in cultural touchstones such as sports to a degree approaching that of male athletes. Sports matter - if they were “just a game”, Russia wouldn’t spend billions to cheat their way to glory.

The US spent much of the 20th century not caring about football while the rest of the world professionalized around it, through a combination of bad luck and sinister plotting, and lots of available alternatives like baseball and gridiron football. It’s one more way in which my country can persist in not caring about the rest of the world, acting like it’s better or can’t be bothered, and it accentuates a propensity toward isolationism and condescension. So to the extent that the success of our women’s team can be a way to get more Americans to care about soccer, to feel good about cheering their country in it, I think it can change hearts and minds on our bonds with the rest of the world. The women’s national team is a winner that’s easy to root for, but they only play a few times a year, a periodic flash in the pan. It’s the regular pro leagues, creating long-term fans and buzz for their teams’ home regions, that will create the change I want to see in the world.

Other people can not care about some or all of those, or care for different reasons, but that’s where I’m coming from here: I want to see the game grow, in the US and globally, but I especially want the US to remain a leader on the women’s side. And it’s with that in mind that I bring you all the good news below.

Women’s Pro Sports Context

Let’s first remember where we’re coming from, and what has driven women’s pro leagues to “niche” status even today.

The Women’s Tennis Association, founded in the 1970s principally thanks to Billie Jean King, took ~20 years to become more than a sideshow. As now famously told in the movie King Richard, Richard Williams was watching TV and saw a $20,000 prize check awarded to a tournament winner in 1978, thought that looked like a pretty good deal, and decided on the spot that he would raise his daughters to be tennis players. 18 years later, Venus and Serena would usher in the era of actual stardom and glamour for the sport, which today while not quite as well-funded as the men’s edition, is viewed about as equal in prestige and given equal TV attention. It is arguably the world’s most established pro sports competition for women. However, the sport suffers from one big drawback: it’s kinda winner-take-all. Serena Williams is a billionaire, but players outside the top-100 are often spending more than they make in tournaments, just to attend and have some minimum of coaching. So by its structure, the sport is a bit of a pyramid scheme, even for the men (and the same is true in golf, to a lesser extent). A few champions become rich, and a bunch of people toil away trying (and mostly failing) to become one of them, with some on the lower rungs even getting preyed on. And like all individual sports, it lacks the long-term identity and fanbase formation of pro sports teams, who play home games in a city and have kids buy jerseys and become talk fodder at backyard BBQs.

The WNBA, meanwhile, was founded in response to women’s basketball emerging in the 1996 Atlanta Olympics, and is a big success by those measures. After semi-serious and semi-funded attempts at a pro league had all failed in the late 70s, mid-80s and early-90s, the NBA used that cultural momentum from the Olympics, plus substantial committed and ongoing investment from their own franchises, to launch the WNBA to much fanfare and quickly put it on a stable financial footing. But after initial crowds the first 3 years (1997-1999) reached 10k paid attendance per game, attendance has plateaued and slowly fallen off, and in 2023 sat at about 6.6k per game:

This dropoff has been buoyed by rising TV contracts and viewership (up 50% in 2021) and other commercial revenue, but it’s fair to say that the league’s financial trajectory is not all that exciting. Up until a few years ago, top players routinely left during the offseason to supplement their incomes playing in better-funded leagues abroad (chiefly Russia and China, whose team owners are happy to deficit-spend for ego reasons). League minimum salaries in the WNBA today sit at $57k, the average salary is $120k, and league maximum is $215k. Given the small-ish rosters of basketball teams, that’s a pretty reasonable bar to clear for a team budget. Nobody playing in the WNBA is impoverished… but nobody is making WTA Top-20 money either, nevermind Serena Williams money. And there’s not much reason to think that will change anytime soon, despite a recent $75M investment and restrictive CBA terms. Now look, getting a million paid butts-in-seats to watch women’s pro teams is still a great achievement, so I am in no way dismissive. But if we’re looking for a sport that’s going to grow past “niche” status and maybe change American culture, you wouldn’t bet on the WNBA at this point, 25+ years in, even if you might have done so in 2000.

The WNBA nevertheless remains the benchmark for financial success in a women’s team sport, sitting at $180-200M in leaguewide revenue for 2023. The competition ranges from slim to grim. World Team Tennis is the epitome of trying to “make fetch happen”. Women’s gridiron football leagues are either criticized for objectifying the athletes, or have low attendance and are essentially pay-to-play, a long way from truly professional. Pro women’s hockey tried starting in 2015 and is about to try again, but they are not yet a venture, nevermind a success.2 And then there’s softball… and while I respect the athletes’ commitment, it’s just hard for me, as a feminist, to take seriously a sport which by design denigrates the athletic capabilities of women by not letting them play, ya know, baseball, like the boys do.3 Rugby, lacrosse, and even ultimate frisbee are out there too, but at best they are semi-pro. All told, the prospects for a legitimate cultural phenomenon emerging from any of those leagues appears dim.

Which leaves us with soccer. The oldest truly professional women’s football league is the Swedish Damallsvenskan, which was first played in 1973 and was the first to go pro in 1988.4 That doesn’t mean “well-paid”, but they were paid, and before long so too were their neighbors in Norway (who won the 1995 Women’s World Cup). Germany and then France were next, with top teams starting to pay players in the 1990s, then gradually saw more of their roster become paid, then more of the mid-table teams paying too, etc. This path toward professionalization was led by a few innovator clubs, above all Olympique Lyonnais (Lyon), driven by a visionary pioneer, OL owner Jean-Michel Aulas. In 2006 he decided to invest whatever amount of money was necessary to have the best women’s team in the world (spoiler alert: a lot was necessary). They have run roughshod over the French league and the pan-European UEFA Women’s Champions League for the decade and a half since, creating lots of Lyon fans even if the wealth was not spread around to other teams. They have been joined in prominence in recent years by Barcelona, and their differing paths were expertly detailed by Yara El-Shaboury in advance of their UWCL Final clash two years ago.

These top leagues have only been “fully professional”, by FIFA standards, for a few years now. In England, the Women’s Super League was formed in 2011 off of the prior amateur leagues, and in 2017 became fully professional. With the backing of the world’s richest football teams (in the Premier League), their players now sport most of the highest women’s salaries in the world (more on them in a minute). Australia launched their pro league, the A-League Women, back in 2008, although it hasn’t grown the way anyone there wants. Mexico pushed its men’s teams to launch companion women’s teams and in 2017 launched Liga MX Femenil, and Japan launched their women’s league to pro status in 2021, and both have had great success in their early going. Along with the US, that’s 8 global leagues that have succeeded in becoming fully pro (USA, ENG, GER, SWE, FRA, JPN, MEX, AUS), with Italy and Spain in the process of making the shift too.5

Pro Women’s Soccer (“WoSo”, to those Very Online folks who obsess over it), as a business venture, has a checkered history in the US too. Although the USWNT dates to the 1980s, it got little attention even after the victory at the inaugural 1991 Women’s World Cup. It wasn’t until the unique cultural phenomenon of the 1999 World Cup team that women’s soccer grabbed a slice of the national zeitgeist. As the USA beat China in the Final in front of a 90,000-strong Rose Bowl crowd that included President Bill Clinton, in dramatic fashion and with an iconic moment (GIF’d!), 40 million Americans were watching on TV. Untold thousands of young American girls were instantly minted as fans, and businesspeople started to think a pro league would be viable.

Launching 2 years later in 2001 with 8 teams, WUSA was our first sincere attempt at that. It lost $100M in 3 years and folded. Top national-team players moved abroad (mostly to Sweden). After 5 years with only amateur competition, in 2009 WPS gave pro another go with 7 teams, again making it only 3 seasons; some owners even treated the whole thing as a gimmick. Off to Sweden went the country’s top stars again, along with Marta, the sport’s consensus Greatest Of All Time player.6 But this time, it was only a year’s hiatus: in 2012, some of the surviving WPS clubs banded together with the best amateur teams for a one-off pro-am league, allowing them a smooth transition when the NWSL began play in 2013. And there they have remained.

Learning from its predecessors’ failures, the NWSL was incubated by the US Soccer Federation itself (plus CAN/MEX), which supplemented its budgets and supplied a lot of its management as it got over its learning curve and hit a level of stability after its first 5 years. The NWSL stopped having USSF perform league management in 2020, let go of the salary subsidy it was getting in 2022, and for the last few years has had a steady growth in attendance while also expanding from 9 teams only 3 years ago to 14 today (and skyrocketing demand to own those teams, driving a huge price surge). As a pharma entrepreneur once quipped, “25 years later, we’re an overnight success”. The league has ever-evolving plans to expand further, in # of teams and in all other ways.

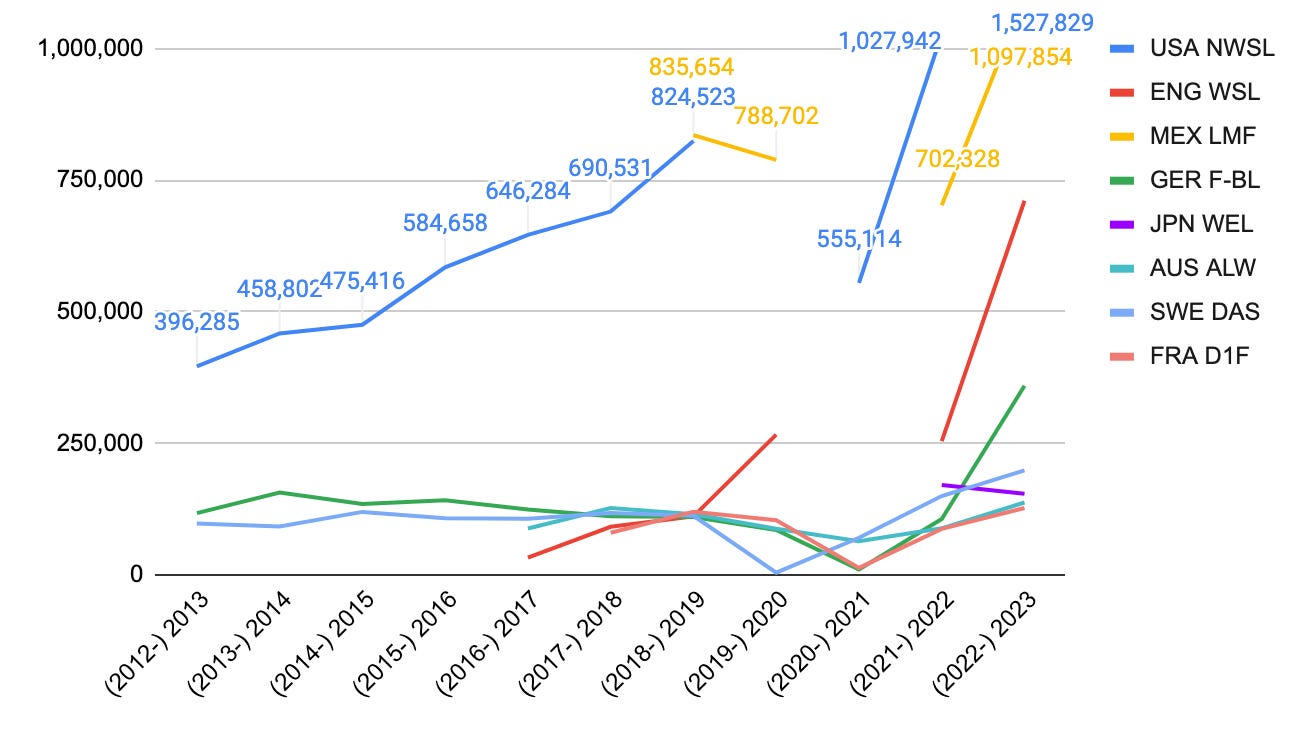

Attendance and the Big 8

The launch of the NWSL happened amid contemporaneous jolts in other countries that helped the rest of those Big 8 (USA, ENG, GER, FRA, JPN, AUS, SWE, MEX) get underway. Japan’s 2011 World Cup win and 2015 runner-up finish pushed their Nadeshiko league to new heights, and so they planned their fully-pro re-launch to happen alongside the Tokyo Olympics in 2021. Germany won the World Cup in 2003 and 2007 and with it came a higher baseline for attendance. All together, we have at least a few years’ attendance data on each of these leagues (though only 3 have data back even as far as the NWSL’s founding), which I’ve compiled from FBRef.com, and it looks like this:

Most leagues averaged 100-150k seasonal attendance for the last decade, up until England (red) made a leap in 2019-2020, with Germany (green) following last year. It might be easier to make sense of it on a “Attendance per-game” basis:

The key takeaways are:

The NWSL has lapped the field at getting fans in the door. Even in their lowest season (2014), they drew better than any other women’s league ever has, up until and excepting only the 2022-23 English WSL.

You can obviously see the pandemic gaps in attendance data. NWSL cancelled 2020,7 and most other leagues ceased reporting attendance (except Sweden) for the 2020-21 season. For 2019-20, numbers are “per non-cancelled game”.

German and Swedish attendance has been stable at ~800-1000 / game for about a decade, up until last year, when Germany took off. Australian attendance is similarly stable, but at a slightly higher number.

Not much WoSo chatter involves the Mexican league, but partly thanks to having an 18-team league, their total attendance is massive, second only to the NWSL, and still #3 on a per-game basis. They actually topped the NWSL in total attendance their second full season (2018-19), an impressive achievement, and they have sustained the momentum in years since. They deserve more attention.

There is an unmistakable jump upwards in the last 2 years, globally. England crowds more than doubled, NWSL went from 5k to 8k to 11k per game, other leagues set new records too. It’s not just re-emergence from the pandemic, it’s a rising tide.

(note that the above numbers include playoffs, if the league holds them - which only NWSL, AUS & MEX do. Wikipedia’s total-attendance rankings page excludes playoffs, which means the WNBA is still tops among women’s sports leagues)

Attendance isn’t everything, but it’s got two things going for it: (1) data availability, courtesy of two high-quality sources8, and (2) objectivity: fans either show up or they don’t. A ticket costs less in Mexico than in the US, but cost of living is lower too - on the whole, it’s a pretty good apples-to-apples comparison of popularity, and nobody can hide from the story it tells.

And man, what a story it tells. Japan’s league launched and was instantly #4 in attendance per-game, though they fell off a bit in their second season. Mexico’s league is massive, which explains why their top teams can pay enough to get NWSL clubs to part with their top strikers (Tigres is reportedly paying Kgatlana $550k / year, which I believe is second-highest in the world right now, behind only Alexia Putellas of Barcelona). The leagues of France, Sweden and Australia are being left behind (the pandemic really crushed Australia’s momentum). And the leagues of England and Germany are rising to challenge the NWSL’s success, after a long incubation period of investment and building the fanbase.

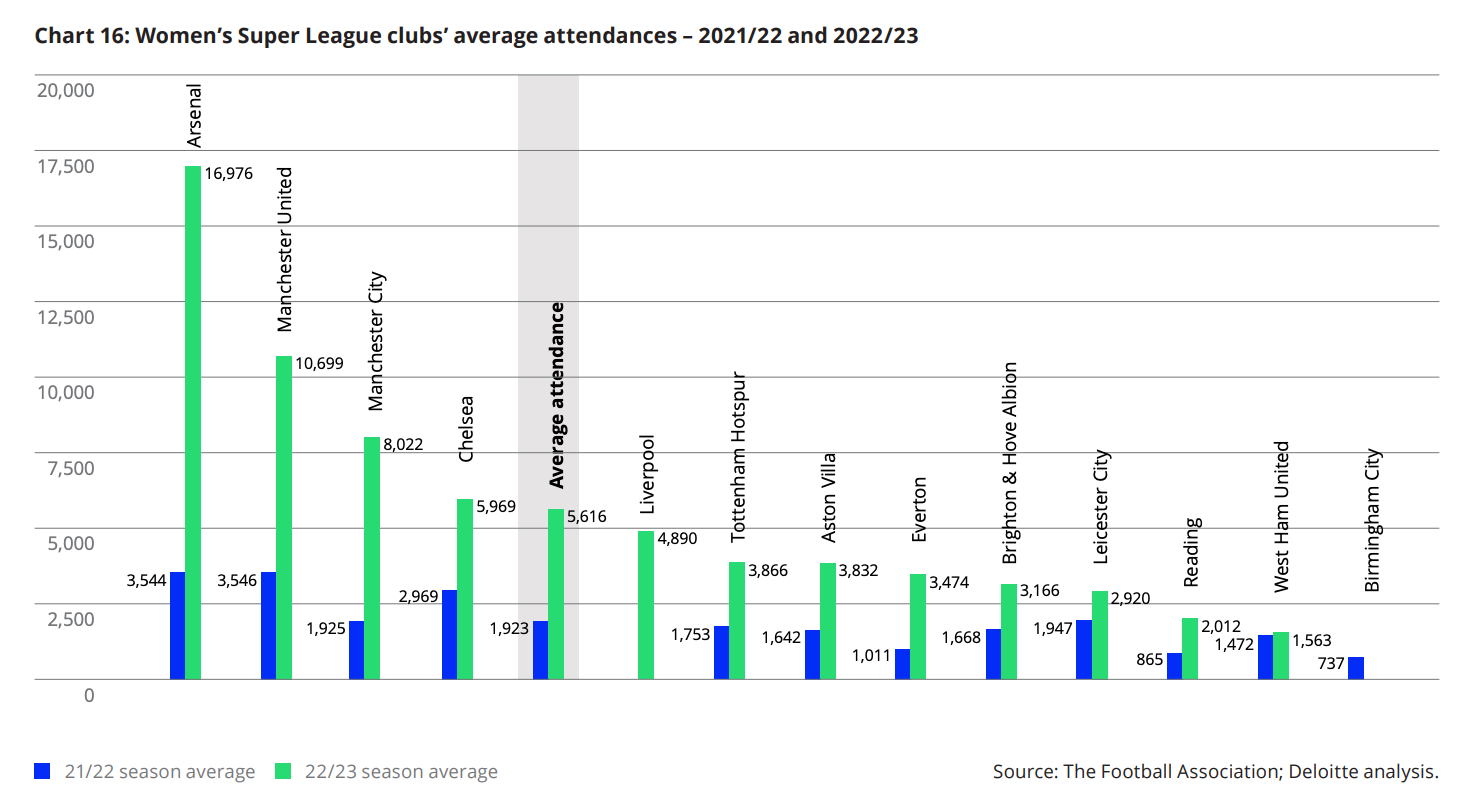

One other thing to note is the bootstrapping effect in most leagues (besides the NWSL) of having nearly all their clubs owned by well-established men’s clubs which have big stadiums. An increasing trend is for the women’s teams to take advantage of that in two ways: (1) having “doubleheaders” at home where the women’s team plays a game and then the men’s team plays, allowing most of the crowd to show up and watch both. And (2) during FIFA international breaks on the men’s calendar, holding women’s games in the men’s primary stadium (e.g. the Emirates for Arsenal, Old Trafford for Manchester United, etc) to give the regular weekly fans something to show up to - which they do, pulling crowds of 20-30k and greatly boosting the league’s total and average attendance. As a result, in 2022-23 Arsenal led the WSL with nearly 17k average home league attendance, despite their nominal home stadium seating only 4,500. These are sustainable tactics helping grow the fanbase9, but we can also see how it’s driving highly-unequal growth10 among the league’s clubs:

At the same time, it’d be hard to overstate how huge the NWSL’s numbers are. More people attended the NWSL’s 2023 season than attended the most recent season of the (comparably-sized) Australian men’s league (A-League). Even if you take their excluding-playoffs number of 10,432 / game for the 2023 season, that beats AAA Baseball handily, it beats the first-division men’s leagues for Belgium (9,600), Russia (9,400), China (9,200) and Australia (7,500), it even beat’s Spain’s Segunda division (10,418)! It’s within shouting distance of England’s EFL League One and the Turkish and Swiss leagues, too. And these leagues have, in some cases, a century’s head-start in building a football culture, massive financial backing and unquestioned “country’s #1 sport” status. At 5,444 per game, England’s WSL is likewise in the range of the first-division men’s numbers for Czechia, Romania and Peru, and near football-mad Brazil’s Serie B (2nd division). The NWSL, in their 11th season, is matching or exceeding the crowd sizes of legit, well-regarded men’s leagues that have been around for many decades. Put that in your pipe and smoke it, Joey Barton.

Revenue

Butts in seats is a nice measure of success, stability and attention. But it’s not the only measure. Arguably even more important is the amount of money each club can bring in, to support growing payrolls, marketing to new fans, additional club coaching and performance staff, and improving facilities. For most clubs, “matchday revenue” (paid attendance / hospitality / concessions11) is a distant 3rd among their revenue channels, behind #2 broadcasting and #1 commercial revenue (sponsorships, events hosting, merchandise, etc - but mostly sponsorships).12

It’s worth mentioning that the data is far more spotty and comes with more caveats than attendance. Many women’s clubs, especially in Europe, are wholly-owned subsidiaries of a large men’s club, which report financial results consolidated at the group level and rarely break out the women’s team separately.13 But we do have some figures to go on.

In “Europe”, the “Eu-” supposedly means “Best-”

Internationally, our best revenue data is from Europe’s big men’s clubs. Among Europe’s big leagues, we have data from 10 out of 12 English WSL clubs, who file separate financial statements for their women’s subsidiaries (West Ham and Aston Villa rely on exemptions to not do so - boo to them). We also have Spain’s Big Two, Barcelona and Real Madrid14. Following the lead of Swiss Ramble, I’ve gone over the financial statements and annual reports and compiled it, and here’s the top-line, comparing Fiscal Year 2022 (2021-22 season) and FY 21 (2020-21 season):

Notes:

Each club has their 2020-21 numbers (left, faded colors) next to their 2021-22 numbers (right, bolder colors). 2022-23 season numbers should become available in March. Clubs that don’t offer a categorical breakdown of revenue have their totals in blue, instead.

These numbers are converted to dollars (RM/Barca from €, the others from £)

Matchday revenues are largely inconsequential; you’d expect that in 2020-21, but only a few have meaningful numbers for 2021-22, which is more surprising.

Real Madrid’s relative paltry revenue is due to their late entry into having a women’s team at all, acquiring a local women’s team only in 2020. Their team payroll, however, is closer to the WSL’s Big 4 than to their revenue peers.

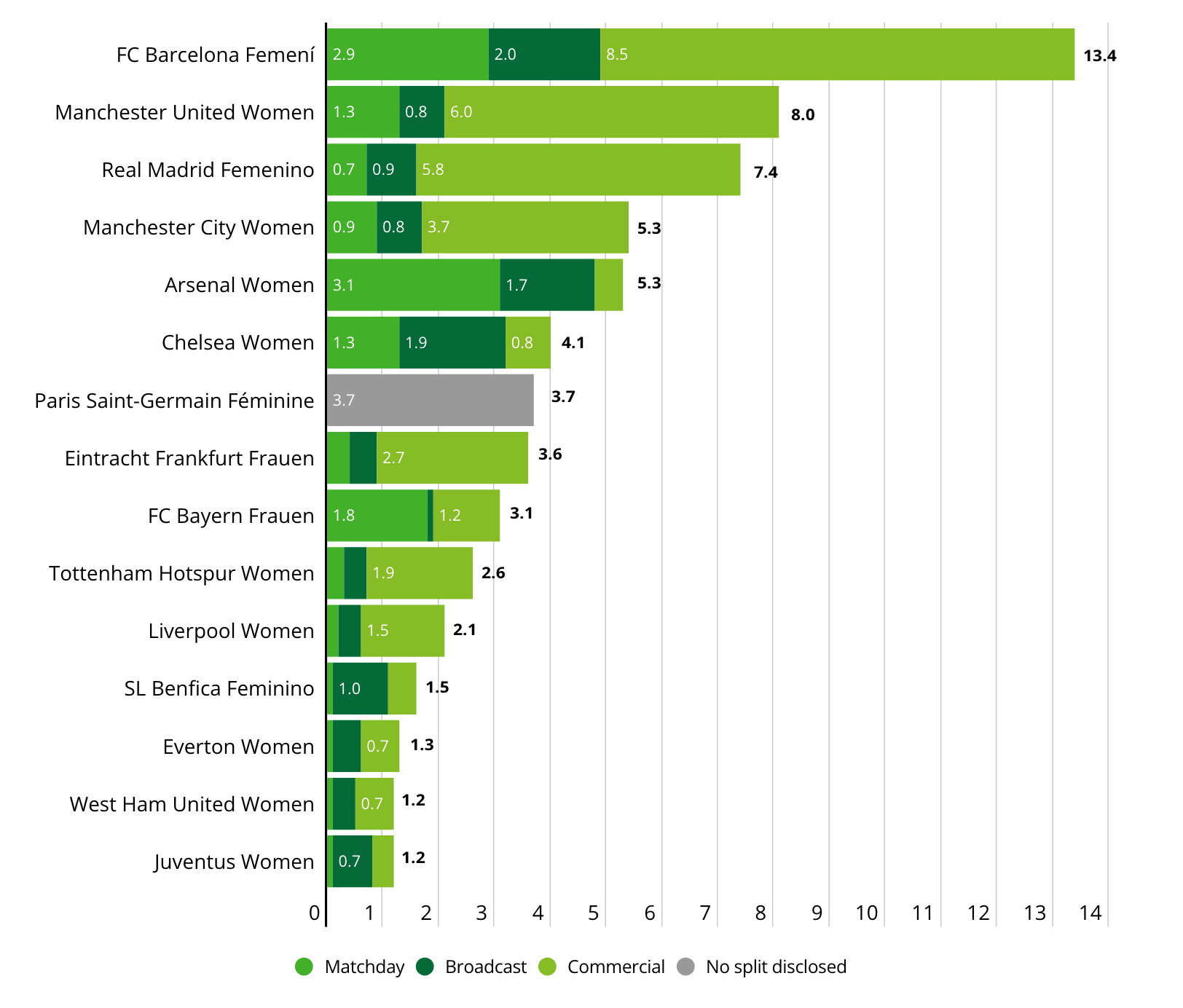

Alongside these financial statements, we also now have reports from Deloitte UK on women’s club revenues. The same group that publishes the “Deloitte Money League”, an annual ranking of (almost all European) men’s clubs by revenue, has started doing likewise for women’s teams (again focusing just on Europe). They add a few 2021-22 numbers to our list: Bayern Munich € 1.7M ($1.9M), WSL missing link West Ham at €1.1M ($1.2M), and 3-time Liga F champ Atletico Madrid at a mere € 0.1M. Their newly-released report covering the 2022-23 season adds a few new names, with one big caveat:

That caveat is that they exclude any contributions from the affiliated men’s club from these revenue numbers, and appear to have done so only penalizing WSL clubs.15 So we shouldn’t regard these as strict equivalents to the previous chart. But it’s still good to ballpark some new clubs (PSG €3.7M, Frankfurt €3.6M, Benfica €1.5M, Juventus €1.2M) while showing strong growth in others (e.g. Bayern up 80% to €3.1M).

Anyway, that’s our baseline: as of a year ago, the biggest clubs in Europe were pulling in $5-9M, and a club generating even $2M was doing pretty well. We happen to know that Barcelona jumped up to $14.8M for 2022-23, and Real Madrid’s published budget expected $7.2M in revenue for 2023-24… but the bottom third of WSL teams are still struggling to crack even $1M in revenue, and dependent on parent-club investment to round out their budgets. In fact, the “Commercial / Other” section of the financial numbers above contains a good amount of grants from the parent club. Only Arsenal has the decency to specify that 74% of its Women’s team’s revenues were parent-group transfers in 2021-22 (and 90% in 2020-21). The others lump it in as part of commercial revenue. But league-wide, we do know that ~40% of WSL revenues are parent-club transfers (per Deloitte’s estimate: £ 13M out of £ 32M league revenue in 2021-22). And we know that the clubs are run at a nontrivial loss: £ 14M collectively for the 12 WSL clubs in 2021-22, which were covered by their parent clubs.

What does “$2M is doing pretty well” really get you, from a budget perspective? If we assume a 70% wages-to-revenue ratio (more on those ratios in a future post), of which 60% is the players, then that’s a $1.2M player payroll. For a 20-player roster, that’s an average of $60k each. Practically speaking, this means half of them are on $30-40k minimums, livable (barely) in your early 20s, and half are making moderate to upper-middle-class money, with probably 1-2 stars pulling $150-200k each. Those minimum salaries may not be glamorous, but you’re still making a living kicking a ball, just the same. So in my mind, that $2M is sort of a threshold for “the club is a viable business” in a developed economy. Below that, and you’re either deficit-spending, or you’re compromising the “pro” part of “we’re a pro sports team”, to some degree.

The second takeaway here is that even in now fully post-pandemic seasons, WSL clubs are not basing their business on matchday revenue. Half the league could play behind closed doors and not notice the money too much. Part of it is because, for the few clubs we have figures from, they’re really not charging much to get in. If we back into an estimate16 for “dollars per fan in attendance”, for the few clubs that itemized their matchday revenue in 2021-22, we see these numbers:

Barcelona: € 1,685 matchday revenue → €7.07 / attendee ($7.67)

Arsenal: £ 532k matchday revenue → £7.27 / attendee ($9.28)

Man United: £ 337k matchday revenue → £8.81 / attendee ($11.25)

Man City: £ 226k matchday revenue → £7.86 / attendee ($10.04)

Tottenham: £ 68k matchday revenue → £3.25 / attendee ($4.15)

Birmingham: £ 23k matchday revenue → £2.43 / attendee ($3.10)

If we take Deloitte’s 2022-23 matchday figures17, this improves, but only a little:

Barcelona: € 2,879k matchday revenue → €10.40 / attendee ($11.27)

Arsenal: € 3,100k matchday revenue → £9.51 / attendee ($12.08)

Man United: € 1,300k matchday revenue → £9.14 / attendee ($11.61)

Man City: € 900k matchday revenue → £9.07 / attendee ($11.52)

Chelsea: € 1,300k matchday revenue → £8.56 / attendee ($10.88)

Tottenham: € 300k matchday revenue → £5.34 / attendee ($6.79)

Even the WSL’s detractors should be willing to admit that the in-person experience is worth more than ten bucks per person. And I think this must include concessions, too. Go sell some beer, guys. Even a little bit.

As for sponsorship deals, although numbers are not often disclosed, one big one is the WSL’s league title sponsor, Barclays. Their deal went from £ 3M / yr (per Deloitte) initially in 2019 to £ 10M / year for the 2022-23 through 2024-25 seasons, strong in both magnitude and growth rate.

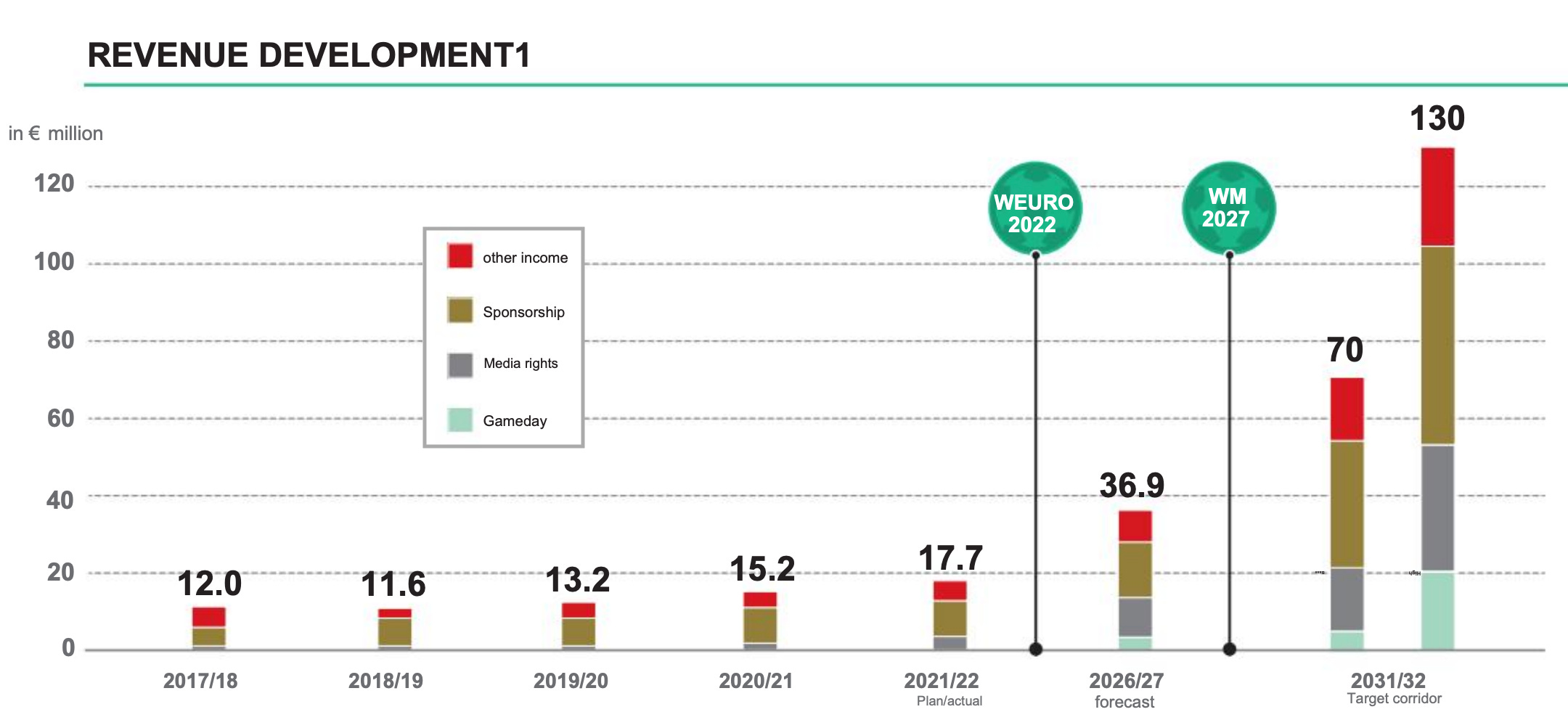

We also have leaguewide revenue data for Germany (that’s the Frauen-Bundesliga). In December 2022, the league hired consultants to project out an optimistic future after a decade of imagined growth. But to do so, they gave us 5 years of history, i.e. total revenue for the league’s 12 clubs, given to them by the DFB:

That € 17.7M for 2021-22 means $19.4M leaguewide, or $1.6M average per club - about 1/2 the WSL’s numbers. But Frankfurt and Wolfsburg (plus Bayern Munich’s € 1.7M, per Deloitte) are probably the lion’s share of that, and I’d expect the curve by-club to look a lot like the WSL’s above, with the bottom few teams running on 300-400k per year. The study also notes that the DFB distributes €3M in centralized sponsorship marketing to the clubs ($272k / club), helpful to the baseline if done evenly. On the other hand, the growth from €12.0M ($13.2M) in 2017-18 is 10.2% annual growth over those 5 years, after being (per the attendance numbers above) largely flat for the decade prior. Yet another signal of the sport’s accelerating growth, even if Europe tends to concentrate the gains among its premium clubs.

Finally, it’s worth discussing the UEFA Women’s Champions League. First held in 2001-02, they started offering prize money in 2011, and finally started offering serious prize money - material to even a big women’s club’s revenue numbers - for the 2021-22 competition.18 Much like the men’s competition, the money has the effect of making the rich richer, locking in a hierarchy of clubs such that a few can always have the best players and win everything, and everyone else begs for handouts. But we can’t ignore those numbers, either (they don’t appear in in clubs’ financial statements, but we can calculate them). Here is the 3-year cumulative leaderboard since UEFA first gave out real money (including only results-to-date for this season):

The list of names doesn’t look all that different from the men’s club pecking order, frankly. UWCL semifinalists each year clear over €1M, all 16 teams in the group stage make over €500k, and those who fail in qualifying get a check that… pays for their travel to compete. Probably. Thanks for coming, guys! Meanwhile, 23% of the prize pool is distributed to non-competing teams in Europe’s women’s leagues, roughly € 100k per country, so figure about € 10k per club. I guess that’s better than nothing, but it’s not what you’d call “a rising tide lifting all boats”, either.

Around the World

The annual FIFA women’s benchmarking report covers league and club finances for ~30 first-division women’s leagues globally. It’s the only solid reporting I’ve found on getting the data we covered above for the less-glamorous leagues. In their 2021 report (and sadly not since), they asked leagues for average-club financial breakdowns by category, for the clubs’ 2019 or 2019-2020 season (the last full pre-pandemic one). They got top-line per-club revenue numbers back from 22 leagues:

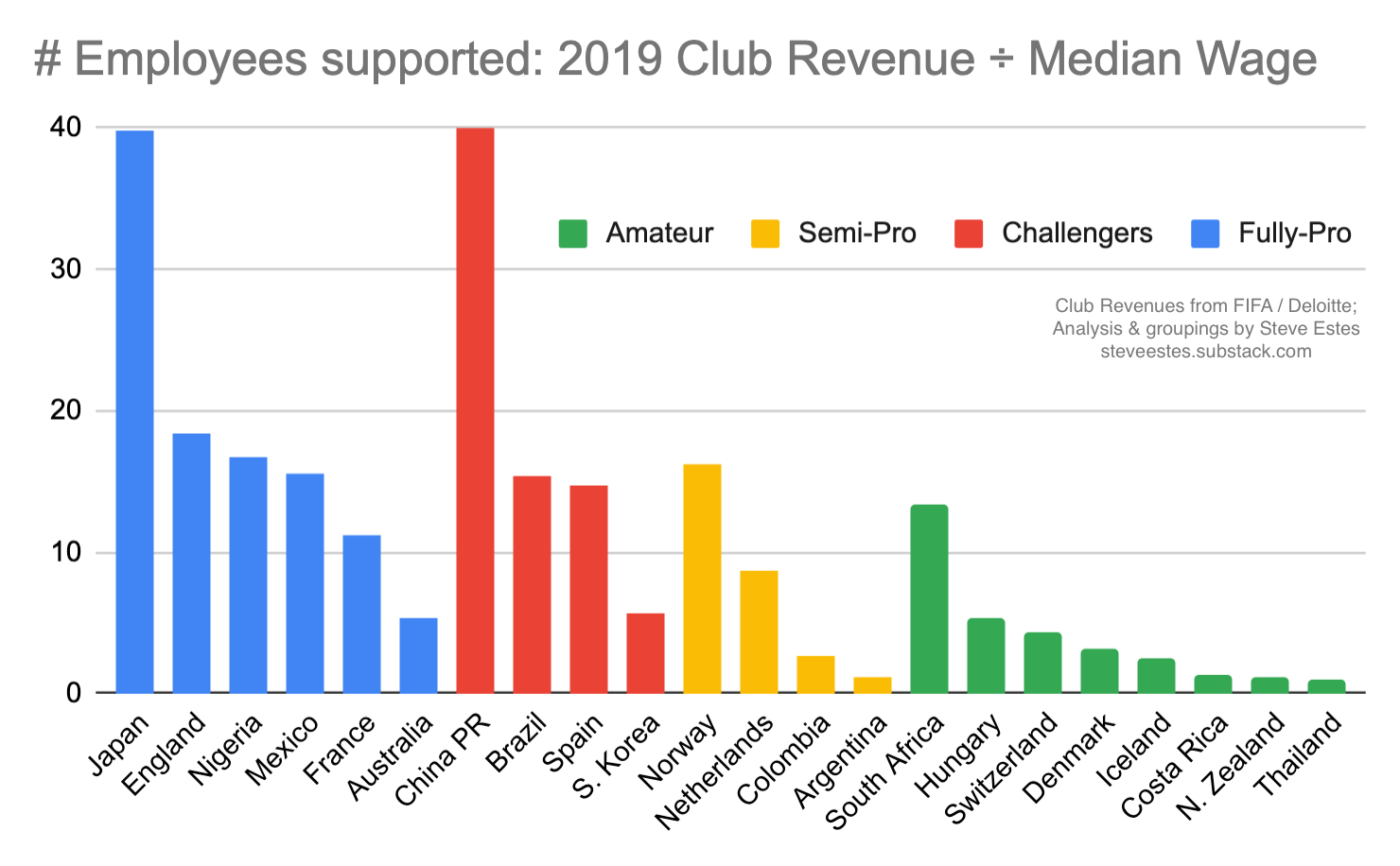

That’s Japan leading the way, ahead of England, Spain, France, etc, two full years before they even shifted their league to be fully pro. Nigeria looks low on a revenue basis, but if you were to divide the Y axis through by the X axis here, and measure “how many country median-wage workers could the club’s revenue support”, Nigeria actually looks very solid, more in line the big leagues:

The groupings here are from another post where we analyze the professionalism level of each league. This shows that the reported average club revenue (in 2019) was sufficient to support 40 employees in Japan, 47 in China (if you buy their numbers), and for most other fully-pro leagues around the world, between 15-20. It also shows that some leagues are financially closer to being ready to professionalize than others (e.g. South Africa, Brazil, etc).

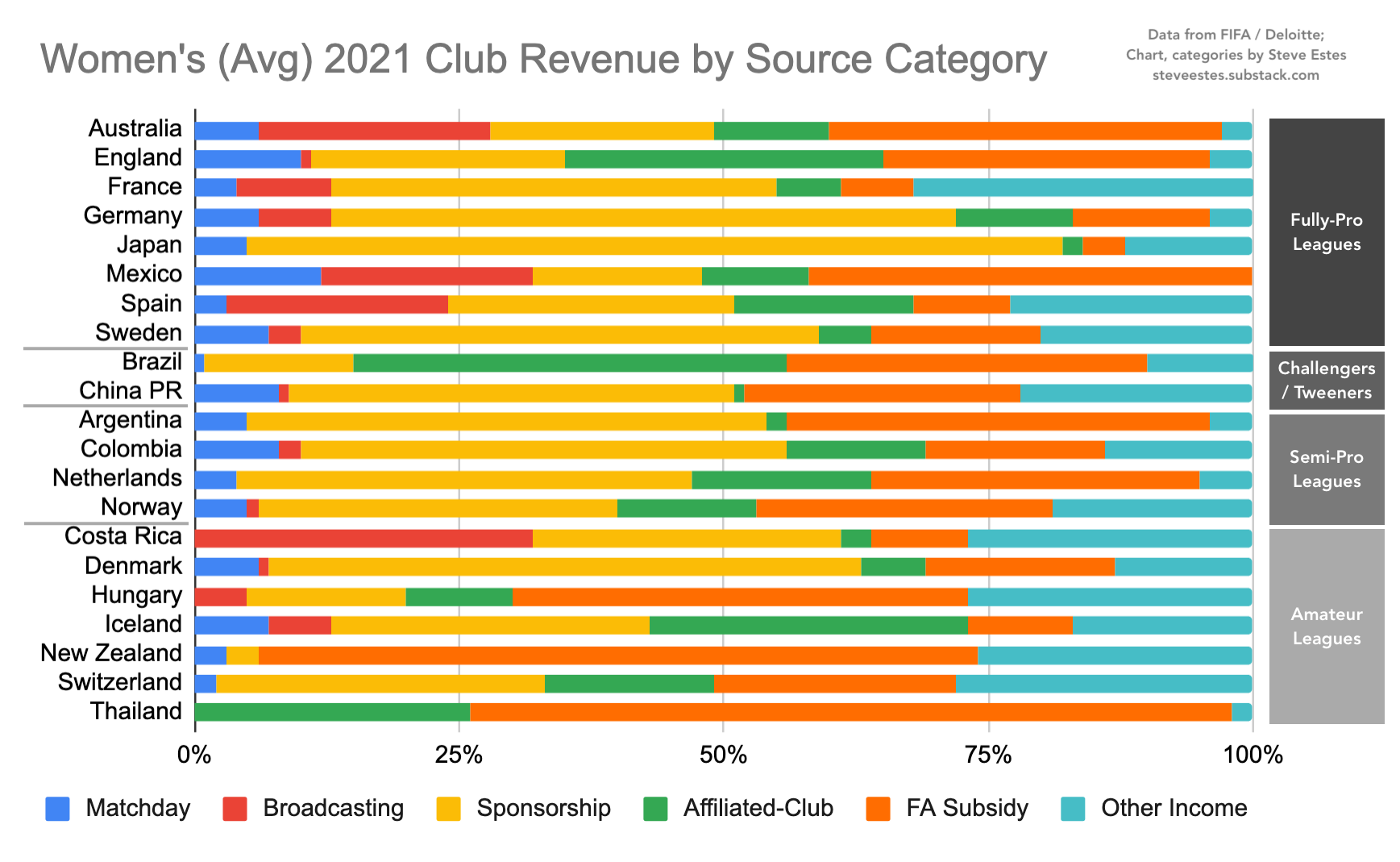

Deloitte also got revenue category-level percentages from 22 leagues19:

This breakdown is fascinating to me:

Matchday revenue is a minor factor everywhere, but relatively, it’s the biggest deal in Mexico (and slightly behind that is England, China and Colombia).

Broadcasting deals are nonexistent in many countries (lack of red bar), and insignificant in plenty more. But some countries have surprisingly important deals: Costa Rica most of all, and Mexico (for all its fragmentation) doing well overall. Australia has had challenges, but still relies on it a lot, and Spain had a great deal before improving it even more last year - details on those are below.

Sponsorship is crucial always and everywhere. But some countries have done a poor job at it, notably Australia and Mexico (among the pros), while others such as Japan and Germany have been leading the way.

Leagues differ substantially in how much their teams rely on subsidies from parent clubs or the FA. In (amateur) Thailand, it’s nearly 100% of revenue, while in Japan it’s merely 6%. Germany and France are “very independent” or “poorly supported”, depending on your point of view - in particular, French men’s clubs being noted money-losing machines surely affects what budget they devote to their women’s teams.

Biggest surprise with club + FA support is how much Brazil’s clubs get: 75% of revenue. Their reputation cuts the other way, that they are not supported well enough to hit launch velocity as a league, which is why their stars all play NWSL. Averaging a mere 400 attendance per game probably is a factor.

To put “affiliated-club revenue” in context, the following leagues giving numbers have fewer than half of their clubs affiliated with a men’s club: China, Denmark, New Zealand, Sweden, and Thailand (and Japan is close). That’s also the case for South Africa, Israel, South Korea, and of course USA, but they did not report here.

Other Income can be varied, but the biggest portion is probably corporate hospitality at games, and hosting events like concerts.

These breakdowns are useful context if we’re looking at the relative financial health of a league, even though the numbers are a bit old and the reporting year itself (2021) comes with a lot of anomalies from the pandemic.

Look out, here comes NWSL with a folding chair!

What do we know about NWSL club finances? Not quite as much, since they’re not obliged to file financial statements in the US. Only what they tell us. But there have been a few glimpses behind the veil, above all Sportico’s annual valuation study. The full study is paywalled, but summaries of it tell us that the NWSL’s 12 teams generated an estimated $112.3M in revenue in 2023, $9.4M per club. In other words, the average NWSL club brought in more money than Arsenal, Chelsea and Manchester United. Here’s Sportico’s per-club estimates:

Note that the revenue numbers are just for the 2023 regular season, so not including playoffs or expansion fees.20 Sportico interviewed a number of insiders for this, and they say that 9 of the 12 teams provided them with information directly, so even though it’s not “official”, I have no reason to doubt it.

Leading the pack was Angel City FC, which entered the league only in 2022, but crushed its pre-launch phase so hard, they should make a business-school case study out of it. They very nearly led the league in attendance in their first season, at 15,513 per regular-season game, and again were a close second in 2023 at 19,756 per game. Those are bonkers numbers, people - MLS itself averages 21k per game. That 19,756 is more than 26 of the 30 NBA franchises! And as you’d expect, Sportico estimates that Angel City led NWSL in revenue in 2023, hauling in $31M last year. Again for the people in the back: THIRTY ONE MILLION DOLLARS! More than double Barcelona’s 2022-23. In their second year of existence.

Heather Pease, then-VP of Ticketing at Angel City, signed up 16,000 season-ticket holders before the first ball was kicked. She is now repeating the trick as Bay FC prepares to launch in San Francisco for this coming season - she’s trying to become the first head of ticketing to be elected to a sport’s Hall of Fame, I guess. I sure wouldn’t bet against her. But tell me that isn’t basically a magic trick, straight-up dark marketing sorcery. ACFC sold $6M in merchandise alone in 2022, leading the league, and $11M in sponsorships, more than 7 MLS teams. Their average ticket price is $41, per SBJ (compared with ~$10 total matchday revenue per-fan for the WSL big-3, above; Gotham FC averages $37). They reportedly had several games where their gate revenue topped $1M, from just that one game. And that’s with Angel City being only mid-table on the field; they clearly have plenty of room to grow further. Part of their secret was bringing in a star-studded cast of celebrities as part of the initial ownership group: “Backed by celebrity investors including Serena Williams, Christina Aguilera, Eva Longoria and Billie Jean King…“. Perhaps not something that your average Topeka FC could pull off. But also not something entirely beyond the power of teams launching in any mid-to-large-size market, in the US or globally.

Another view of NWSL revenues comes from Seattle via the French Alps, as Reign FC was bought by Olympique Lyonnais in 2019. Buried deep in OL’s financial statements is a breakout P&L for OL Reign.21 2022-23 on top, 2021-22 below it:

I don’t fully grasp the distinction here between “Revenue” and “Operating Revenue” - maybe OL will reply to my email - but it looks like Reign made either $5.6M or $6.0M in 2021-22, and then in 2022-23 (splitting two NWSL seasons) made either $8.2M or $59.8M. Which is a difference worth inquiring over, to say the least. I suspect “Operating Revenue” includes some allocated money from the group level, so that the real figure is closer to the $8.2M. But still, this is an official document filed with the French government, not some second-hand analyst report, so it confirms the ranges we’re discussing. That $8.2M would, again, be more than any team in the English WSL made in 2021-22, and Reign’s $5.6M in 2021-22 would’ve been 4th in the WSL. And the actual number might be a lot higher than that, if the real explanation is something like “Operating Revenue includes the windfalls from NWSL expansion fees”.

Broadcasting

While WSL clubs aren’t dependent on matchday revenue (or seemingly all that interested in it), much more important to them - and knowable for us - is TV broadcasting. And same goes for every league around the world - they want reach (recruit new fans) as well as the guaranteed revenue stream. Deloitte observes22 that the 2015 Women’s World Cup Final got more viewers in the US (25.4M) than did that year’s finals for the NBA or NHL, and the first match of the 2020 NWSL season got 3x the viewers of any previous one of their matches. Audience size and media rights pricing are tightly linked, and both are trending positively.

The WSL’s current deal, running from 2021-22 through this 2023-24 season, pays £ 8M / year ($9.8M), according to the Daily Mail. There is a 75% / 25% split between WSL clubs and second-division (Championship) clubs. Of the season’s 132 matches, Sky broadcasts 35 per year, and BBC another 22; even with more than half the league’s matches not broadcast, viewership is up 45% this season so far. With the deal expiring at the end of the current season, TNT is rumored to be bidding for the new one. The WSL is targeting a £ 20M / yr ($25M) figure for the forthcoming deal, a 150% jump from the current. If so, the annual share to each WSL club would be $1.6M, which by itself would be a sizable revenue floor, even for teams without much commercial or matchday revenue.

Comparing the TV rights deals (in $USD) among the Big 8 leagues + Italy & Spain, here’s what we see:23

The Frauen-Bundesliga’s media rights were recently renewed last summer, jumping from € 325k / yr (yes, for the whole league) to € 5.2M / yr (or $473k per team), still well behind peers but at least the same order of magnitude, and importantly, at least 4 of 6 weekly matches will be broadcast - they’ve probably sacrificed getting top dollar in order to invest in reach. But even at the numbers they’re getting, given the estimated revenue for the bottom half of the league, this deal should double it and make the playing field a bit less tilted.

Doing equally well for themselves is Spain, which actually had 2x bigger deal than NWSL did from 2019-2021, and managed to bump that up to nearly $500k per club last year (more than Germany, 3rd behind NWSL and WSL). Italy, by contrast, is sticking with short-term deals in the hopes of seeing numbers climb faster; The Athletic puts Serie A’s current deal around €1M / yr, not bad for the league’s first year of going pro.

In Australia, the most recent rights deal bundled the Men’s and Women’s leagues together, with Viacom CBS inking a 5-year deal at AUD $40M / year (USD $27M / year) that also saw them take an equity stake in the leagues’ parent company. There’s no way to disaggregate those numbers to get a number for what’s going to the women’s clubs, without seeing the business strategy documents for the league. If you assume the women are getting a 20% cut, the per-club annual amounts would be respectable (~$400k USD); hopefully that’s not too optimistic. However, Australia is the only one of the Big 8 leagues that bundles women’s rights like this. Adding insult to injury, one year into the current deal, the broadcasters pulled the one weekly free-to-air women’s game due to poor ratings and put the whole league on streaming.

France’s leagues are marketed by their FA, which is a proven incompetent at marketing media rights. True to form, they went to market in April 2023 for a package that would include D1 Feminine plus the women’s national team, then abandoned it in May after getting poor results, split off the NT + WWC rights in June and extended their (poor, ~€ 1M / yr) domestic rights deal with Canal+… for six years. While adding streaming over DAZN, with terms not disclosed, which means nobody wanted to brag about them. If D1F were a stock, I would short it.

Almost equally disappointing is Japan’s WE League, which signed an 8-year streaming deal with DAZN. Financial terms were not disclosed, making it likely this is an in-kind deal (DAZN produces the broadcasts at their own expense; the league neither pays nor receives money for it though). That’s fine to get a new property established for a few years, but committing to that for 8 years - without a domestic free-to-air or even cable TV broadcast partner to boost audience reach - suggests more self-doubt and lack of ambition than the league’s (quality) attendance numbers would otherwise justify.

Sweden had probably the world’s first 7-figure broadcast deal for a women’s league, paying $1.2M / yr ($98k / club) from 2011-2015. Their latest deal, inked in 2022 with Viaplay, splits the content between TV broadcast and streaming, but represents only a slight bump in total fees, to $1.94M / yr (~$140k / club). Worse, Viaplay has big financial struggles, having overpaid for Premier League rights. But the Swedes put up big viewership numbers for women’s football; it’s still a good market.

Mexico’s rights are not sold centrally by the league; clubs are still cutting individual deals to show their women’s matches, such as Chivas with Telemundo. They are the only one of the Big 8 leagues to not market TV rights collectively. League management knows this is an issue and is seeking to change it.

All of which is (perhaps excessive) prelude to the elephant in the room: This past fall, the NWSL struck colossal new media rights deals for the next 4 years, going from $1.5M / yr in their previous 3-year deal with CBS to a collection of deals with 4 broadcasters that will net the league an absurd $60M per year. That is north of the annual fees for the men’s leagues of Sweden, Argentina, Austria, etc, and within range of Russia and Turkey. That is an average of almost $4.3M per year per club beginning 2024, guaranteed before they sell the first ticket, jersey or sponsorship. The WSL is hoping, with their forthcoming new deal, to get to a number (£ 20M / yr) that would be only 37% the size of NWSL’s current one. NWSL has lined up “go build our own stadiums”-level money, and I’m sure that very thing is part of the strategy they shared with broadcasters to get them to part with such sums.

So, bottom line, NWSL is blowing away the competition, financially. And although we’re not going into it in this post, you can see the results of that in their latest Collective Bargaining Agreement and the evolution of team payrolls, working environment, a decline in players having side jobs / offseason gigs, and so on.

Team Valuations

One last signal we should be paying attention to is how much the teams themselves are worth. While it doesn’t benefit the fans, and only very-indirectly benefits the players, the growth of the value of an owner’s investment shows two things: (1) the bet they made is paying off, and consequently (2) there’s greater demand for owning women’s football teams, pushing up the price that they’re sold for. With that growth also comes increases in the amount those owners are willing to invest into operations and facilities.

For teams owned by a parent (men’s) club, as with the WSL, we never get a real valuation of the women’s club - they’re just willing to deficit-spend to build and grow it, often for social-equity / public pressure reasons. Even most of the independent women’s clubs in Europe (like Turbine Potsdam) are still clubs, they’re nonprofit social groups run by members, and they want to build community first, and generate financial returns second (or not at all). But teams founded and run as if they’re a social obligation probably won’t reach the scale to achieve the kind of social change I’d like to see, either. So let’s see where the smart money is betting.

First, expansion fees. The USA’s major sports leagues charge new owners a substantial fee in exchange for being granted a franchise in their league, with the NWSL following this practice too. The original teams for the NWSL’s 2013 launch were selected by US Soccer, but expansion fees were apparently $1M up until 2019. Racing Louisville became the 10th team in the league for a fee “between $1-2M” in 2019. When Angel City and SD Wave were awarded franchises, they paid $2M and $5M respectively in 2020. WoSo observers knew it was only a matter of time before those numbers climbed. Having sold and relocated the Utah Royals back in 2020, in 2023 the new RSL ownership exercised a $2M option they held to re-establish the team, but by that point demand had exceeded supply: In advance of their entry into the league, Bay FC paid a $53M expansion fee in early 2023, as part of a total founding investment of $125M, and the forthcoming Boston team paid $53M as well, committing an equal amount to stadium improvements.24 They were apparently the winners out of more than a dozen bids, with offers still being explored for the 16th team to enter with Boston in 2026.

Team sale prices tell a similar story. The years up through about 2019 were fairly grim:

Sky Blue FC was founded in 2006 and 2/3s of ownership bought by NJ Governor Phil Murphy; by 2016 his tax returns showed he had lost $5M on the team.

The Western NY Flash, an NWSL founding club, won the championship in 2016, and were then promptly sold to NC businessman Steve Malik and moved to North Carolina to become the Courage. No terms were reported, but the league’s press release cited the greater market size for NC; we can assume they were losing money.

In 2017 the then-oldest professional women’s team, the Boston Breakers, had their (all-male) ownership team suddenly decide not to back the team for 2018, and attempts to find a buyer at $5M were unsuccessful; the team was folded and the players dispersed, alongside reports that the team had been behind on its payments to the league since 2014.

FC Kansas City had its owners give up on it after 2017, was moved to Utah through 2020, and when that owner was forced to sell, it went back to KC for $5M; their new owners are building the first women’s-sports-specific stadium in the world, pouring $135M of their own money into it and a training facility.

In 2019, the founder of Seattle Reign FC moved the team to play in Tacoma for want of a suitable stadium situation, and in ever-greater need for operating capital, later that year sold 89.5% of the team to Olympique Lyonnais in a deal that valued the team at only $3.5M.

Everything changed when, in early 2022, Washington Spirit minority owner Michele Kang pulled a boardroom power move to muscle toxic team owner Steve Baldwin (who had been reluctant to accept her buyout offer, seemingly out of spite) out of majority ownership. She became majority owner, to the widespread acclaim of players and league observers. Her valuation of the team at purchase was $35M (and 18 months later, Sportico values it at $54M, a tidy bit of work by her).

Angel City launched with a long list of celebrity investors, led by celebrity couple Serena Williams and Alexis Ohanian, and in April 2021 raised their Serie A funding round at a valuation of over $100M, per Sportico. Their multi-stream revenue strategy has, obviously, set new records. 2.5 years later, Sportico values them at $180M, by far the most valuable women’s sports team in the world. A torrent of transactions in the tens-of-millions have followed the last few years, now with valuations being disclosed, which means someone was proud enough to leak them:

The numbers being thrown around may not make present-day sense from a cashflow standpoint; instead, they represent a bet by sophisticated investors that there is tremendous untapped growth opportunity. Sports Business Journal quotes a sports investment banker:

“Are these numbers justified by typical financial valuation analyses and revenue multiples? Probably not. You can’t get there on a cashflow basis or revenue multiple,” said Chuck Baker, co-chair of Sidley Austin’s sports and media practice. “It’s all about the upside. Given how long the holding period tends to be and how infrequently these teams trade, investors are bidding on long-term appreciation.”

The NWSL’s teams are designed to run at breakeven, investing whatever cash they bring in into facilities, staffing, marketing and so on to capture that growth (not to mention a rise in player payrolls). Investing in growth today can mean growth of the team’s valuation at a higher rate than just sitting back and taking profits now. Anyone familiar with the growth curve of Venture Capital-backed investments will recognize the similarities.

For a league that’s only a few years removed from the Red Stars’ owner running around with a wrench to personally fix the plumbing in a player’s apartment, these numbers may seem bizarre and surreal. We’re talking about a league that appointed a new Kansas City owner in 2017 and then cashiered him after just one year of mismanagement, sending the team’s players and assets to Utah. But the culture shift is coming from replacing owners who perhaps had more social-justice motivation than business sense (or scummier motivations), who for whatever reason just weren’t equipped to be first-class sports owners, with new ownership who are professional, disciplined, and have deep pockets to invest where needed. The best example might be the move from sketchy former Utah owner Loy Hansen - who was forced to sell both his Salt Lake City teams - to new owner David Blitzer, one of the world’s foremost sports owners, who is now exercising the option granted him at that acquisition to re-establish a Utah NWSL team for 2024. That evolution of the general quality of ownership may make the experience of being a fan more “corporate”, but it need not be, as Angel City is testament to. It’s just part of the maturity / learning curve of the sport itself.

Up in Canada, the long-awaited launch of a Canadian women’s pro league is being touted with franchise costs of “between $8-10M”, with the founder pointing to NWSL valuations to argue that as a good deal (as of Dec 2022, though she hasn’t gotten less right since then), and lining up significant sponsorship deals even prior to launch. So for those trying to make the business case that women’s football is a good investment, the NWSL stands as a beacon of proof.

Beyond the NWSL, there are not many opportunities for growth-motivated investment, but among those that exist, Michele Kang is seizing many of them. In May 2023, it was reported that she was buying 52% of OL Féminin, Lyon’s famous winners of many a UWCL title. This means assuming the team’s reported € 12M in annual losses. She’s doing this by placing her 80% ownership of the Washington Spirit into a holding company that will also own OLF, with Lyon owning the other 48% (and thus becoming a minority investor in the Spirit, effectively). For that reason, OL is selling the now-rebranded Seattle Reign (probably to the Sounders), and expects to get about $50M for the team. Details of her transaction are complex, but explained in OL’s financial statements.25 Kang announced that she planned to buy more teams, forming the first multi-club ownership group in women’s football (a trend on the rise in men’s football, most famously with City Football Group). True to her word, late last year she bought out the only fully independent club in England’s top-two divisions, the Women’s Championship team London City Lionesses, who had accumulated about $2M in losses since their owner launched them in 2019. She has ambitious plans to share training techniques, research and infrastructure among a global family of clubs.

Kang’s acquisition of OL Féminin also gives us the one “sale of a big European women’s club” data point to compare to the NWSL franchise values above: In OL’s financial statements, the valuation of their stake in the new holding company - effectively the value of the team as of May 2023 - was $29.3M for the contribution of the team, and another $9.6M for contributing a 50-year license agreement from the club to allow OLF to continue to use the OL brand, facilities, etc (basically so they can still be “Lyon”, even if they’re now owned by a third party). So Lyon, titan of European women’s football, is worth roughly as much as what the NWSL’s least valuable team, Chicago, just sold for.

Headwinds and Struggles

The above paints a very rosy picture for the sport in general and the NWSL in particular, for both fans, players and owners. But we can’t cover the topic without at least mentioning some of the darker sides (or at least negative signs) of the sport as well. At the root of many of them is, of course, sexism in its many forms. Its manifestations include:

Abuse, both verbal and sexual, of athletes by coaches and training staff. The Utah Royals were sold and moved to KC in 2020 after sexist abuse by the Utah owner moved the league to compel a sale. After complaints and a 14-month investigation, the NWSL banned 4 coaches for life in early 2023. A parallel report by US Soccer reported that such abuse often begins at the youth levels. The report spurred players to speak up in a number of other countries about how they’d faced similar things, with perhaps no situation more brazen than the Zambian national team coach… until the trophy ceremony at the end of the Women’s World Cup, when the Spanish FA president kissed a victorious player on the lips, without the slightest hesitation (or consent). The good news is, at least in the NWSL, that there hasn’t been a recurrence of bad news of this variety in over a year. For a sense of how such issues are discussed by soccer fans, read here.

Although not rising to the same level of criminality, objectification of the players as sexual objects, rather than as professionals and athletes. This practice of course has a long inglorious history, but manifests even today with top players like Aston Villa’s Alisha Lehmann. There’s no pleasing the bros: reject the importance of attractiveness too much and you get branded as a “butch” league, sport or player; lean into it too much and the attention you get is all the wrong kind. Dress codes that maximize revealing outfits (for the TV ratings, they say) are common in other sports, and even in soccer, stars often feel an obligation to wear lots of makeup.

Even in the absence of abuse, paternalism regarding women players abounds. The conditions that led the Spanish FA president to make the “kiss heard round the world” were set by an atmosphere that thought nothing of having infantilizing rules for their team, such as odd curfews where they had to leave the door open for the team’s head coach to talk to them.

Bundling of sponsorship deals and broadcast rights with a club’s men’s team or a league’s men’s division, in a way that makes the women a throw-in rather than something the sponsor / broadcaster explicitly wanted and valued (in monetary terms). As detailed in Deloitte’s report, 10 out of 12 WSL teams have primary jersey (kit) sponsors that are the same as the men’s team, and it reflects a relative lack of focus on trying to generate revenue specifically for the women, and line up brand value and messaging strategy accordingly. It’s a rule in business that if a seller treats something as if it has no value (even if it does!), buyers and consumers will react and treat it accordingly. While among the top professional leagues, only Australia bundles TV rights this way, in up-and-coming leagues it’s more common, such as Israel, Nigeria, the Netherlands, and South Africa.

Particularly among teams affiliated with a larger men’s club, the overwhelming gender split of having men’s coaches in the women’s game (while, spoiler alert, there are no women’s coaches in the men’s game, though they’re getting closer). Women’s football has sometimes been treated as a jobs program for excess men’s coaches, rather than as a discipline that coaches should specialize in if they want employment, one requiring different skills and a nuanced appreciation for the ways in which the women’s game is different.

Lack of investment in the teams, in areas from housing, travel, training facilities, and other areas - Sky Blue FC had no working toilets in 2018. Even when co-owned by a men’s club, teams often have only second-class-citizen status for using those facilities. Part of this is the economics of the teams themselves, or limited resources of owners, but part is apathy.

These (and many more flavors of it) are part of what women’s sports is combating through its survival and growth. It’s part of why it’s so culturally important for them to succeed on their own terms, to create a beautiful sporting product that can be appreciated for the game itself.

Although sexism is intertwined with the vast divide in economics between the men’s and women’s game, the latter is worth mentioning on its own. I’m not one who will point to the gulf in revenue and compensation numbers vs the men and say that’s per-se evidence of sexism; rather, I think it’s important to recognize that women’s football is a different game, and in the entertainment landscape, “you eat what you kill” - money going out the door must be proportional to money coming in, or you’re running a charity, not a business. Compensation is a consequence of eyeballs watching on TV, online or in-person, not some decision that can be made independently of the budget if the powers that be would just start valuing women more equally.

And that explains why following the finances is worthwhile, because WoSo becoming “real money” will give both the space and the impetus to find fixes to the above. That’s why so much of this post focuses on the positive financial trends, even if I could talk more about the CBAs and growth around the world. As women’s football becomes less of a niche thing for people to watch, or to appreciate as just another sport one can enjoy, along will come the money, the respect, and the better treatment.

Thanks for reading.

I will mostly call it “football”, unless it’s a proper name, just because it’s impossible to follow the game globally and not feel more comfortable calling it that than calling it soccer. There’s nothing wrong with saying “soccer” (the Aussies prefer it too!), but if one is going to adopt certain English or international terms around the game and reject some others, the name of the sport (You play with a ball! Using your foot!) seems like a pretty easy choice to accept. Whereas I will carry on saying “field” and not “pitch”, using “sideline” and “end-line” and not “touchline” and “by-line”, etc. I will not apologize for code-switching, and neither should anyone. :)

Edit: The new PWHL has launched since initial publication of this article, and I am compelled to note that, by the size of the recent crowds, I was clearly too skeptical. They have drawn an average of 5k in their first 13 matches, including 13.6k for Minnesota’s home opener, a record. And they have nontrivial salary floors through the work of their players association. I’m definitely hoping they continue making a fool out of me on this point.

Yes, men play softball too, and the women’s leagues went on a while, but there’s no getting around that the sport looks like a Fisher-Price version of the real thing. Girls are still allowed to play little league, up until they get to a certain age and then they’re gently nudged into softball. Call me when high schools establish girls’ baseball teams, instead of just using softball to meet Title IX obligations - until then, I take a dim view of it.

WUSA claims to have been the first women’s league where all players were paid, but I think they’re wrong, I think it’s Sweden. See this study. That said, per-game attendance was super low until 2002, as were salaries (all but the top stars had side jobs), but they got checks.

I don’t want this to be too Euro-centric. In another post I’ll show some evidence that women’s leagues in Cameroon, Nigeria and Morocco probably deserve inclusion on that list, and Peru, and Brazil and Tanzania are starting to make a case too. But the real money - in terms of attendance and investment and running on budgets that aren’t “shoestring” - is principally in those 8 leagues right now, with Italy and Spain racing to join them. Also, the data on them is better - I can’t really analyze those African leagues the way I can the rich-country ones. I hope that changes soon. Italy and Spain’s leagues went fully pro only in 2022-23, and while there are some promising trends, the data services have not caught up yet on them either.

It’s not a coincidence that Sweden (and then Norway) were the first to have pro women’s leagues, or that they were regarded among the best in the world until much-larger countries got their WoSo act together. The Nordic countries routinely rate as the most feminist countries on earth (2023: 4 of the top 5!). This dates back to the Viking times, where under customary Viking law, women were subjects, whereas in traditional Christian law, women were objects (i.e., property). It didn’t mean they were equal, but they were treated as people, having both rights and agency, which for historical times counts as massively progressive. Those cultural roots have been sustained in many realms, sport being one of them - and feminists might argue the correlation to being the happiest countries on earth, too.

Fun fact: the league saved its pandemic season with a PPP loan from the federal government, which gave it the funds to pay players without any teams folding (detailed in Keh & Das, 2020).

Aside from FBRef.com, I’m very indebted to WorldFootball.net, which is a publication of the Helm-Spiel football data service. Nobody else seems to have comprehensive WoSo attendance numbers.

While the use of the men’s stadium for occasional featured games isn’t a “gimmick” - it’s clearly repeatable and bringing in money - those matches don’t speak to the depth and loyalty of the fanbase quite as much as independent clubs drawing bigger crowds on their own merits. For example, the NWSL’s average attendance in 2023 (11,152) was 107% bigger than the English WSL’s in 2022-23 (5,387), but the median attendance (the “middle” number if you lined them up in order) that season for the NWSL (8,515) was 175% bigger than WSL (3,102) - meaning that the WSL’s attendance is more heavily weighted towards / dependent on those featured matches, and weighted towards the biggest clubs. Same skew goes for Germany: NWSL-to-FBL average attendance is 3.1x, but median attendance is 4x. Median attendance does tell you something important about the financial sustainability of the non-glamour clubs in a given league.

This is from Deloitte’s June 2023 report, p35. And no, I can’t account for why it’s reporting a ~230-per-game higher number than the data services like WFB are reporting. When in doubt, though, I tend to trust the auditable source (WFB and FBRef give game-by-game numbers that can be checked against media reports). Of that ~30k difference in total attendance, Arsenal is reporting +20k of it, Man City +9k, Man United +6k, Everton +5.5k, and Brighton, Villa and Reading between -3 and -4k each. And Wikipedia is somewhere int he middle (e.g. here’s Arsenal). Beats me, guys, maybe they were working off only preliminary data. I just included the nice visualization of year-over-year growth, because it saved me the trouble.

In measuring the revenue numbers of men’s clubs, Deloitte considers “matchday revenue” to include gate receipts / hospitality, but also “membership revenue” - i.e., the clubs charging people an annual fee to be a member, which in some countries confers meaningful voting rights. It should be thought of as an analogue to a gym membership, since some of these clubs are indeed recreation facilities for members, not merely a pro-sports team with some historical baggage. In the NWSL, though, “member” is just a friendly term for season-ticket holder, even though it often comes with additional perks.

Not on that list, you might observe, is income from player transfers. Deloitte’s UK-centric coverage of women’s football makes a big deal of that topic, as does FIFA’s (Deloitte-prepared) annual benchmarking survey of women’s teams and leagues. But in 2022 there were a grand total of 98 women’s club transfers that involved economic compensation - most of them for very small money, even if there are a few publicized exceptions. And even in the men’s game, player trading is essentially a zero-sum or even negative-sum game (once you account for agent compensation, taxes, etc). A few men’s clubs reliably generate income selling players, but summed across the entire game the net transfer fee is zero, thus for a club to make a profit with it, another has to take a loss / net expense. So we’re going to ignore that market function / revenue stream here, despite its prominence in the men’s game - it’s not a sustainable channel for growth of the sport.

It’s worth noting that not every women’s club is a subsidiary of a men’s club. England’s London City Lionesses (2nd-division but professional) became independent from Millwall in 2019, and just got bought by WoSo entrepreneur Michele Kang. England’s second-division Lewes women’s team does have a men’s division, but it’s seventh-division and amateur, so the women’s numbers are basically the club’s numbers. And there are teams in other leagues - like Essen and Turbine Potsdam in Germany - which are standalone women’s clubs, but I’m unable to find financial statements from them. In France, D1F’s FC Fleury 91 has a men’s section that is 4th-division (amateur), so I’m hoping to dig up their club statements too. Every other D1F club is affiliated with a Ligue 1 or Ligue 2 professional men’s team, though. D2F has a few, including ESOF, but the second division is not fully professional. In Italy, Como is fully independent, and Pomigliano has only a Serie D (semi-pro) men’s affiliate… but God help you with trying to find Italian corporate financial statements if the club doesn’t post them on its website.

And, annoyingly, that’s all I could find. I tried REAL hard, guys. I emailed a bunch of clubs from Sweden to Italy, I was google-translating 200-page annual reports in half a dozen languages, combing through footnotes and stuff (like you’re doing right now!). Best I got besides the above was staffing numbers for Ajax’s women’s team (surprisingly high, like Barca/Lyon numbers of employees). But I’m sure in the coming years, more and more clubs will start reporting their women’s teams as standalone business units. In particular, I expect European hegemon Lyon (OL Feminin) will soon have independent financial reports, as Michele Kang has bought part of the club and they have jointly moved it to its own operating entity. That’s the biggest fish we know nothing about, financially. Anyway, the only place I didn’t really look was Japan. If anyone knows Japanese and can find club financial statements, DM me, we’ll geek out over it.

Excluding affiliated-club contributions is fair if it’s just direct transfers (analogous to an owner making equity contributions to keep things afloat), but if it’s an allocated share of a joint sponsorship deal, imo that’s reasonable to count as women’s-club revenue. It’s also done inconsistently by Deloitte: Barcelona’s numbers here (€13.5M) are identical to the reported figures from their financial statements, so no discount was taken off them for any shared sponsorships, despite knowing that they have some, including Nike and Spotify. Only the WSL clubs seem to have been given that haircut. So we’ll have to wait a few months yet for clubs’ 2022-23 published financial statements to get a clearer picture of year-over-year growth.

For 2021-22, this calculation starts with league home attendance per match, adds in the known # of non-league matches (FA Women’s Cup, UWCL, etc), assumes the attendance for those is the same average (it’s not, some UWCL matches get put in Premier League stadiums and average a lot, but for most matches it’s close), gets a total annual all-matches attendance estimate from that, and then divides reported matchday revenue by that attendance. This excludes preseason and friendlies.

These numbers are only ballpark. For 2022-23 we have full attendance numbers from Wikipedia + WorldFootball, including for FA Cup + League Cup, so attendance is accurate. However, matchday revenue as reported by Deloitte is only rounded to the nearest € 100k, so it’s not very precise, particularly when revenue numbers are low. For Everton and West Ham, Deloitte’s numbers were only €0.1M, i.e. 100k, which could be anywhere from 51-149k and still round to that number; so, we’ve excluded them from the list.

Where applicable, competition prize money is grouped into a club’s “broadcast revenue” category, if they break it out. At least, according to Deloitte - the clubs’ financial statements don’t really make much mention of it, for the handful of clubs where it’s relevant.

20 of the 22 countries were the same in both lists. South Korea and Nigeria provided top-line average revenues, but not category percentages; Germany and Sweden provided revenue category breakdowns, but not dollar totals.

Sportico makes no mention of any transfers from parent clubs, as Deloitte does for the WSL. But of the NWSL’s now-14 clubs, only 3 (Orlando, Houston and Utah Royals v2.0) are owned by MLS teams; 2 more have 2nd-division USL-Championship owners (Louisville and North Carolina), which are not exactly awash in cash. Counting OL’s ownership of the Reign, the other 8 teams are fully independent. Whereas, of the 12 WSL clubs last season, 11 have EPL parents, and the 12th (Reading) got relegated, so it’s clearly a big determinant of success. Which is not to say there’s anything wrong with owners funding the operating losses of women’s teams, whether those owners are big established clubs or just rich founders - they’re investing in growth. That’s good! I just have issues counting that deficit spending as “revenue”, and wish it were treated as equity capital.

They don’t break out numbers for OL Féminin, their all-conquering flagship women’s team, but they do for Reign… go figure. They’ll probably start doing so as part of Michele Kang’s new ownership entity, though.

Lots more viewership figures at that link, if interested. Tracking that was beyond my scope here, mostly because they usually seem anecdotal and it’s hard to line up apples-to-apples numbers from year to year to see the trend.

Worth noting that the biggest player in media rights for women’s football is British sports broadcaster and streaming service DAZN. As of Sept 2023 when they secured co-exclusivity to D1F (France), they held domestic broadcast rights for the top women’s divisions in Germany, Spain and Japan, and global (foreign) rights for the UWCL and NWSL plus Spain’s Liga F. Last summer they also acquired ATA Football, which held WSL and D1F streaming rights, a year after acquiring Eleven Sports which held rights to a large diversity of women’s competitions. A big part of their strategy seems to be to sublet some of their match rights to other services like ESPN+, or put them out for free on YouTube (though they’re moving away from that), so their reach is not quite as limited as “streaming” might normally suggest.

Which leads me to a question I have no answer to: Where do those expansion fees go? OK, yes, to the existing teams, probably split evenly. But I mean, what are they used for? Just operating expenses? Could the league keep them to capitalize a loan facility for building stadiums, or starting academies? I see like 30 articles out there about the sheer size of these recent expansion fees, but nobody explaining to me how it’ll matter, other than the signaling of investment value. Help me, Steph Yang, you’re my only hope.

OK fine you sickos, here’s the full story, in before-and-after ownership structure charts. Before last May, OL owned OL Féminin outright, under their “association” (nonprofit public-service group that runs an actual recreational athletic club, plus the youth teams, etc - basically everything that isn’t trying to make a profit), called OLA. The association has an agreement with OL SASU, which is a for-profit “sports company” that runs the men’s first-team (and tries to make money), the terms of which allow the men’s team to use the logos and brand of OL, the club, which has been around for a century. That sort of agreement is common in Europe, not that different from Germany’s 50%+1 rule. Michele Kang happened to already own ~6% of the entity that bought OL, alongside also owning 80% of the Spirit:

Here’s the “after” structure:

As you can see, they made a “NewCo” (which will be called Kyniska Sports), which will now hold MK’s interest in the Spirit, as well as 100% of OL Feminin, the team. Ownership of NewCo is 52% Kang (for contributing the Spirit), 36% OL (for contributing OLF, the team), and 12% to the OL Association (OLA), for contributing its 50-year brand licensing deal to let OLF continue to play as “Olympique Lyonnais” even though they’re no longer directly owned by OL. Of particular note is that asterisk: OL’s shares are non-voting. So they’re along for the ride, will get a share of economic returns if and when a team is sold, but until then, it’s entirely Michele Kang’s show to run as she pleases.